Insurance is one of the largest expenses individuals have regularly, coming in at hundreds, if not thousands of dollars a month for each person. Such high costs warrants that most individuals, especially teens, should understand what insurance is and how it works before they start taking on that expense. Although the math behind insurance payment calculations is complicated, insurance policies have the same fundamentals.

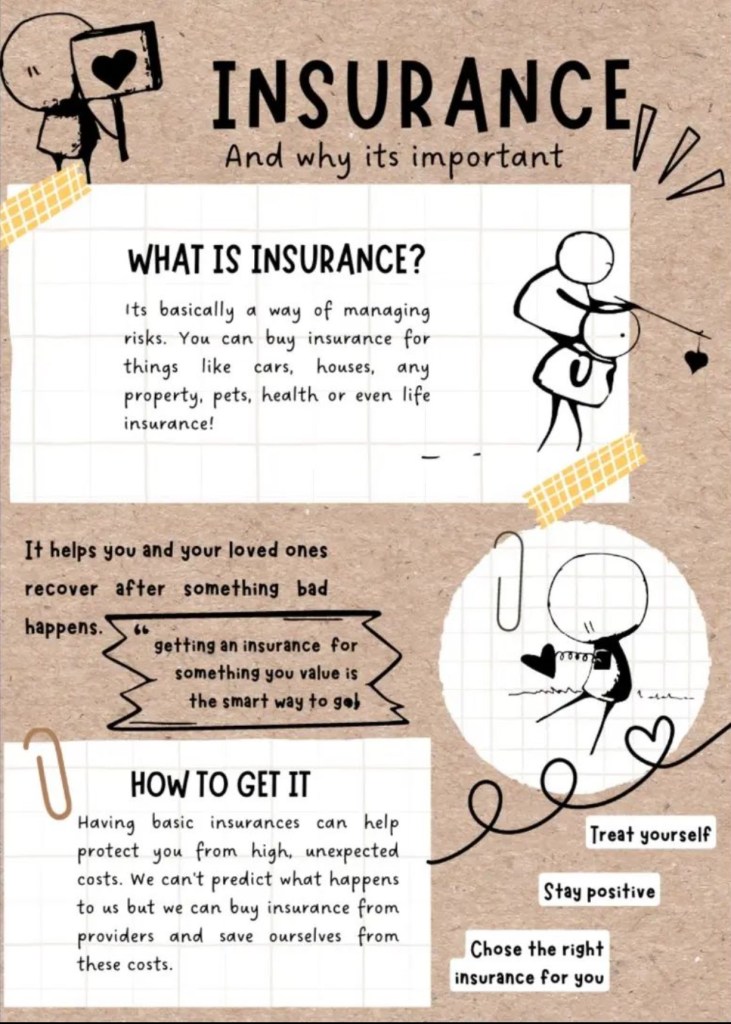

Let’s start with the basics: What is insurance?

Insurance is a way to limit your financial liability through potential times of loss. In Layman’s terms, you are paying someone a bit of money every month now, and in return, they will give the money back when you need it most. Essential terms and parts of insurance everyone should know:

1. Premium: Premium is the monthly payment made for an insurance policy. Premium amount will differ based on many factors, from the type of insurance to how reckless the applicant has been in the past.

2. Deductible: Deductibles are the amount of money you must pay out of pocket before filing a claim with the issuance company to cover damages or loss.

3. Policy limit: The policy limit is the most amount of money an insurance company will pay for damages, based on your selected policy. There can be multiple sub-components of this based on the kind of insurance you have.

4. Copay: Copay is a fixed amount the policy holder has to pay whenever they get a service that is covered by insurance. Copay only kicks in after the entire deductible amount has been paid and is mainly available in health insurance.

5. Exclusions: Exclusions are parts of services or scenarios that are not covered by your insurance, despite it seeming that they should be.

6. Riders: Riders are optional add-ons to an insurance policy. Although these will increase your monthly premiums, the increase can be your worth it

It is important to understand that each of the elements of insurance given above will vary based on your lifestyle and risk appetite, the insurance company, and even other elements listed above. The math behind the pricing can get quite complex but the basics of insurance aren’t, and it always pays off to be aware before having to handle it all by yourself.

Aniket Joshi

Mission Saksham